Discover the truth behind canceling credit cards in this informative blog post. Many Americans have common misconceptions about canceling a credit card they no longer use. Find out the impact of canceling credit cards and gain valuable insights on managing your credit wisely. Don’t miss out on this essential information for financial health.

In this informative blog post, we explore the common misconceptions that many Americans have about canceling a credit card they no longer use. Discover the impact of canceling credit cards and gain valuable insights on managing your credit wisely.

Table of Contents

Canceling a credit card account may seem like a quick fix to limit your overspending or cutting costly fees, but it may come with unintended consequences.

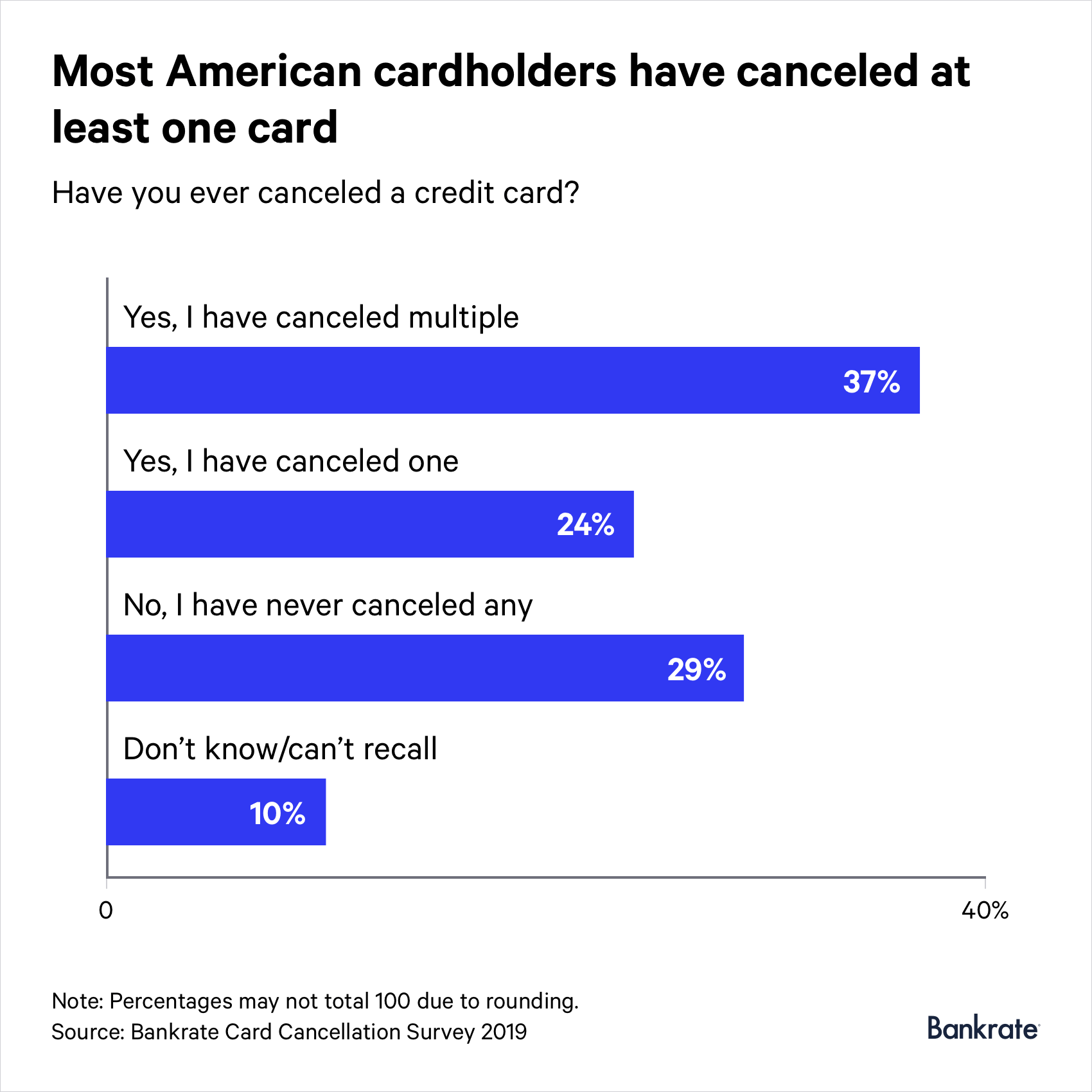

A new Bankrate survey of 2,582 adults, including 2,301 credit cardholders, finds that 61 percent of American cardholders have canceled at least one credit card. Thirty-seven percent of those cardholders have canceled more than one card.

Older generations are more likely than younger cohorts to have closed accounts: 72 percent of baby boomer cardholders have canceled at least one card, compared to 61 percent of Gen X cardholders and 50 percent of millennial cardholders.

Card cancellation misconceptions

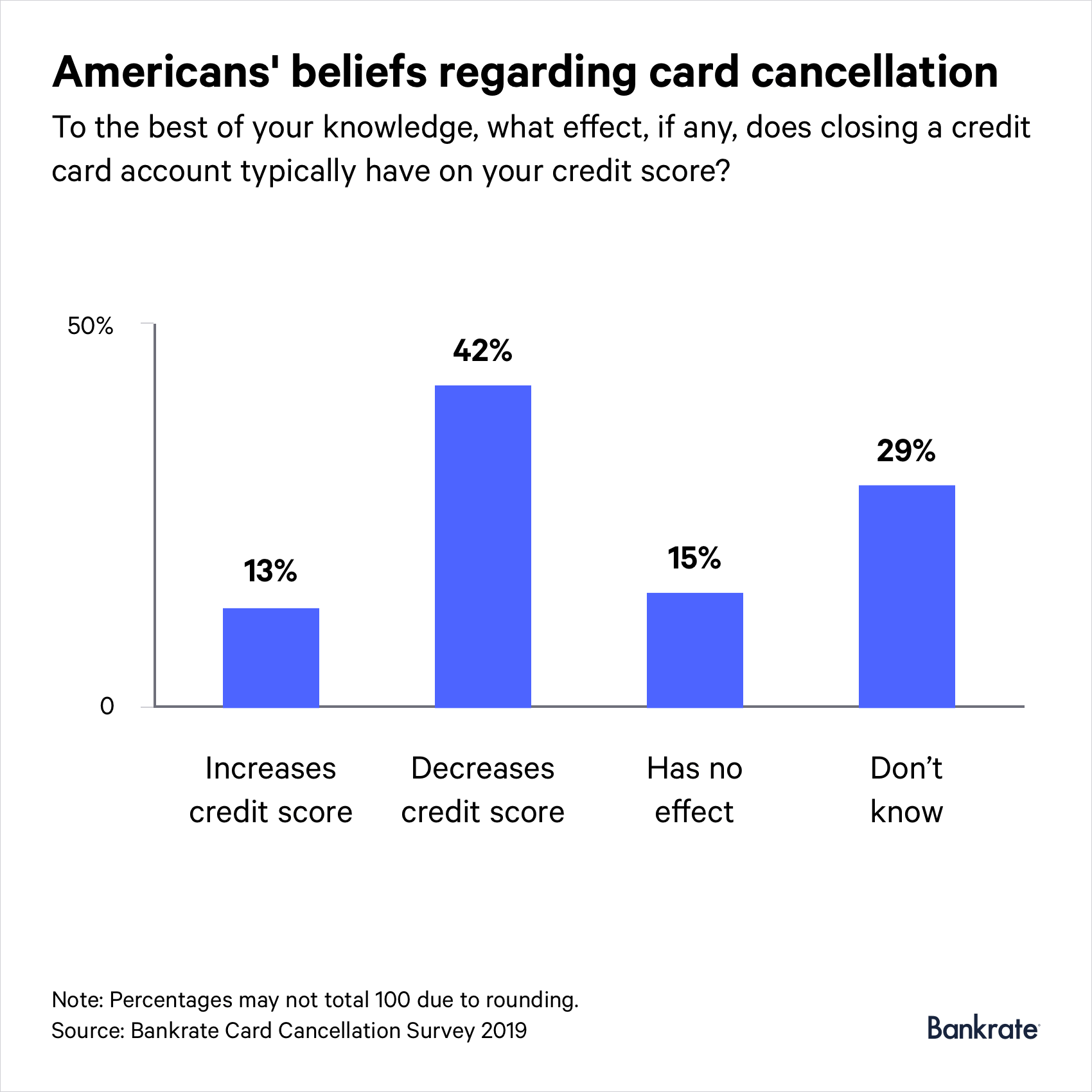

Of cardholders surveyed, just 42 percent correctly assume that canceling a card typically decreases your credit score. Fifteen percent believe it has no effect and 13 percent said closing accounts increases your score. Twelve percent of Americans who have canceled a card in the past even say they did so with the hope of improving their credit score.

Lines of credit contribute to the factors that scoring models like FICO and Vantage Score use to determine your creditworthiness, like credit utilization and average age of accounts. Often, youll not only receive no score benefits from canceling a card that contributes to these factors, but you may see a negative effect.

You should keep old accounts open to boost your credit score, because scoring algorithms look favorably upon long-standing accounts and more available credit, says Ted Rossman, industry analyst at Bankrate.com.

How closing an account may impact your credit score

At 29 percent, many survey respondents simply dont know the impact cancellation may have on their credit score.

While an account that was recently opened or that has a minimal limit may not have serious impact, [c]losing a card that has been open a long time shortens the average age of your credit history when it comes off your credit report, says Amy Thomann, head of consumer credit education at TransUnion. Your credit utilization rate, or the percentage of available credit youre using, may increase if you close a credit card, because you could have less total credit available to you. You may especially see an impact if you keep high balances.

According to Tom Quinn, vice president of scores at FICO, the degree to which your score may be impacted by a closed account depends on your profile.

Its going to be determined based on the consumers use of revolving credit: how many credit card trade lines they have, how many balances, whats the spread between the balances and the available credit, he says. Where its going to have the biggest impact is the closing down of that credit obligation where there is a large and high dollar amount credit line.

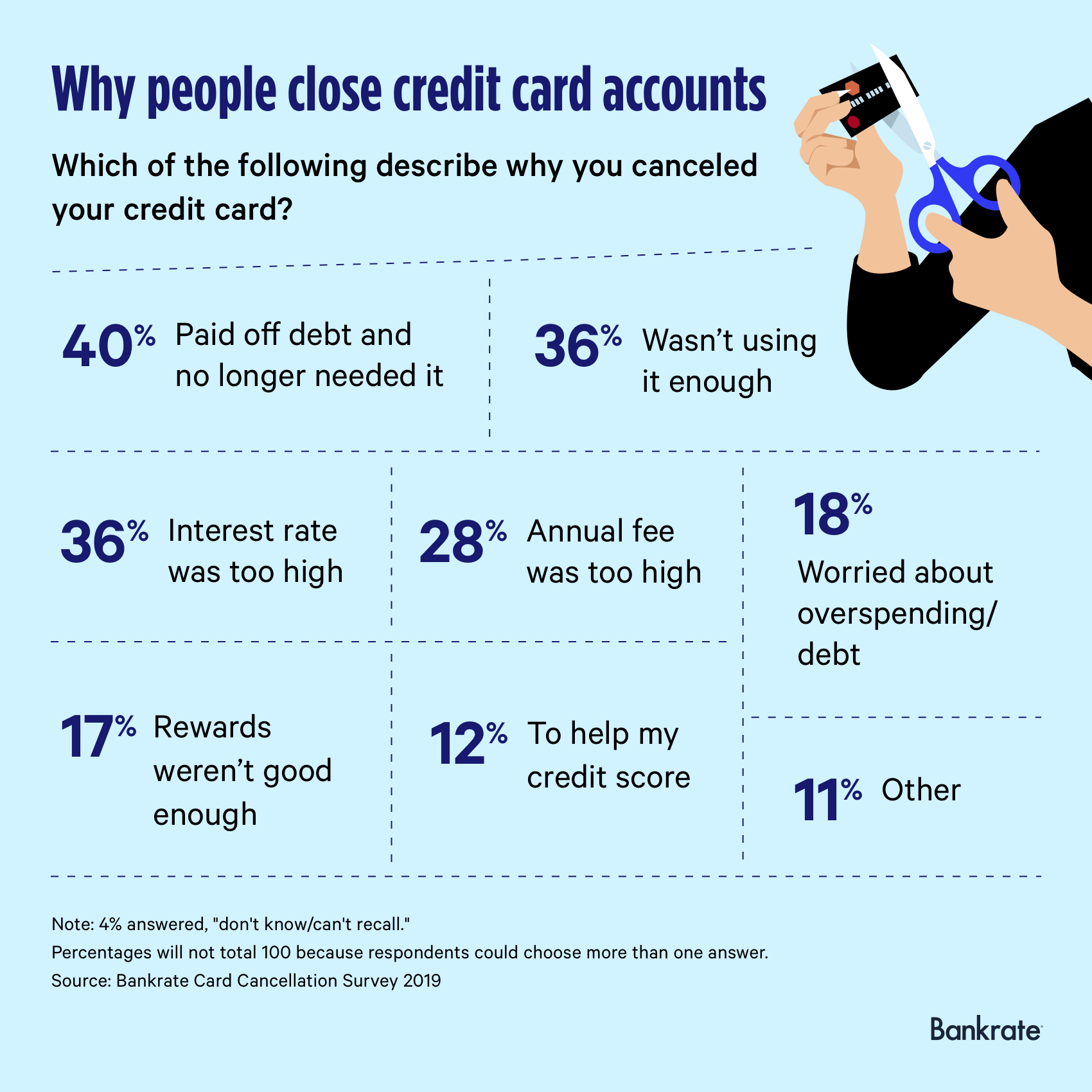

Why do Americans cancel credit cards?

The most popular reasons Americans choose to cancel their cards range from having paid off debts (40 percent) to not using the card enough (36 percent), high interest rates (36 percent) and high annual fees (28 percent).

Millennials, at 25 percent, are more likely than older generations to cite subpar rewards as their reason for closing an account. Generation X, at 31 percent, is most likely to point to high annual fees. Baby boomers (41 percent) and the silent generation (49 percent) are most likely to say they closed an account because they didnt use it enough.

Actions you can take instead

In some instances, closing an account may be beneficial for consumers, Quinn says. If youre already in debt and dont have the discipline to not spend, for instance, limiting that temptation by canceling the card is more important.

But for most, its better for your wallet and your credit score if you refrain from closing accounts. Generally, youll see positive impact on your credit score if you keep long-standing credit cards open and pay off the balances, if any, in full each month, Thomann says.

If youre considering cancellation for any of the most commonly-cited reasons above, here are a few alternative solutions to consider:

Paid off debts

Paying off your credit card debt is a feat in itself, but that doesnt mean you should then forgo credit use altogether.

From a credit score standpoint, I would still leave that card open, Rossman says. If its a balance transfer card, its probably not offering you the best rewards, so keep it open in the background.

Before choosing a balance transfer card, look into options that will serve you best once the balance is paid. One card that Rossman recommends is the Amex EveryDay® Credit Card from American Express*, which offers not only zero percent interest on balance transfers for 15 months with no balance transfer fee (15.24% 26.24% variable APR thereafter), but also 2X Membership Rewards points at U.S. supermarkets on up to $6,000 in spending each year, 1X on everything else and a 20 percent point bonus every time you use your card 20 or more times in a billing cycle.

Keeping a card open isnt an excuse to take on more debt, though. Make sure youre paying off your balance in full and on time each month to build your credit and keep from incurring interest.

High annual fee

If you applied for a card with an annual fee that you can no longer justify, the solution may be as simple as speaking with your issuer. Issuers will often work with you to find a solution that doesnt involve fully closing your account and putting your credit score (or their interest in keeping you as a customer) on the line.

If youre paying an annual fee for a card youre not getting much value from, ask the issuer to downgrade you to a card that does not charge an annual fee, Rossman says. A product change like that will not hurt your credit score because it maintains the account history and credit line.

Check out Bankrates guide to the Best No Annual Fee Cards to narrow down your options.

High interest

If youre using your credit cards responsibly and paying off balances each month, interest rate shouldnt be a factor.

Make your own personal credit card rate zero, Rossman says. With interest rates averaging near 18 percent, carrying any balance is too costly. Youve got to take it upon yourself to manage it properly. Thats what we ultimately want to see: everyone out of debt and maximizing their rewards.

If you do carry a balance though, and the rate on your card seems too high to make a dent in your debt, consider using a balance transfer card to pay it off. Otherwise, start work on improving your credit and keeping up a healthy payment history, as good habits may help you negotiate a lower interest rate with your issuer.

Not using it enough

If you dont pay an annual fee or incur any other expenses and you pay your balance in full each month, theres nothing wrong with keeping an inactive account open.

I would view it as more additive rather than subtractive, Rossman says. Tastes change, and its often in your best interest to compare cards in order to ensure youre getting the best offer on the market for your needs. But you dont have to close your old cards when you find a new one.

Not only can it improve your credit utilization ratio and length of your account history, but you never know when the cards perks may be useful. Maybe it has roadside assistance perks or rental insurance. Maybe its the only card in your wallet with no foreign transaction fees. A card may still be of use even if you dont use it regularly.

If nothing else, keep it simply for the benefit of your score. If you dont need a credit card, but it has a high credit limit or has been open a long time, you might want to keep it open and use it to make small purchases that you pay off on time so you dont affect your score by closing the account, Thomann says.

*The information about the Amex EveryDay Credit Card from American Express has been collected independently by Bankrate.com. The card details have not been reviewed or approved by the card issuer.

Methodology

Bankrate.com commissioned YouGov Plc to conduct the survey. All figures, unless otherwise stated, are from YouGov Plc. Total sample size was 2,582 adults, including 2,301 credit cardholders. Fieldwork was undertaken on May 1-3, 2019. The survey was carried out online and meets rigorous quality standards. It employed a non-probability-based sample using both quotas upfront during collection and then a weighting scheme on the back end designed and proven to provide nationally representative results.

Thanks to Source: https://www.bankrate.com/finance/credit-cards/credit-card-cancellation-survey

canceling credit cards