Learning how to build an emergency fund is the first step to getting your finances in order. You’ll sleep better with some cash in the bank and, most importantly, you can start focusing on longer-term (and more exciting) financial goals.

You probably know that you need to build an emergency fund. But how big should it be, and how can you actually save that money? In this guide, you’ll learn all there is to know about emergency funds — including some advanced financial planning tips that can help you build one quickly.

Table of Contents

What Is An Emergency Fund?

An emergency fund is money that’s set aside to cover unexpected expenses. Common uses for emergency funds are car and home repairs, medical bills, and as insurance against reduced earnings or job loss.

The most common place to hold your emergency fund is in a high-yield savings account, although some people also utilize money market accounts. Money market accounts can return a higher APY, but as they’re a form of investment account they do come with a risk of loss (albeit a relatively low one).

Why You Need An Emergency Fund

The primary benefit of having an emergency fund is that when unexpected expenses do happen — and they certainly will — you can handle them without significant changes to your current lifestyle.

On a basic level, having an emergency fund allows you to afford a car repair so you can get to work, or to get your HVAC fixed if it breaks down during the middle of winter, without having to take on revolving, high-interest credit card debt that you’ll be paying down for years.

But those are just the first-order benefits.

An emergency fund can make you feel more secure with your finances. It can alleviate the need to sell an investment in a down market (the absolute worst time to liquidate it). And it can even allow you to take advantage of unexpected opportunities, such as covering the moving expenses for a surprise job offer in a new city.

And here’s a personal example: if I hadn’t had an emergency fund, I wouldn’t have left my job to go full-time with this site.

How Big Should Your Emergency Fund Be?

The general rule of thumb is that an emergency fund should be equal to three to six months’ worth of expenses.

But a phrase you’ll hear me repeat frequently is to make personal finance personal. Instead of relying on rules of thumb, let’s dig a bit deeper to determine the right size of emergency fund for you.

The benefit of a large emergency fund (six months, for example), is that it provides better protection against financial catastrophe. This includes worst-case scenarios like a long-term layoff in a down economy.

But the downside to carrying that size of emergency fund is the opportunity cost. Specifically, you’ll be earning a very minimal amount on your cash, even with a high-interest bank. If you carry a small emergency fund, you can invest more in an IRA or a 401(k) with an employer match, which will provide a much better overall return.

Another issue I have with the three-to-six-month emergency fund rule is that it doesn’t take into account what your income and expenses would be after an emergency occurs.

Let’s use our worst-case scenario of a long-term layoff in a down economy. Also, let’s say that your current monthly expenses are around $5,000 per month.

If you were laid off, could you reduce that $5,000 of monthly expenses relatively quickly? Say by cutting all your subscriptions, reducing eating out to absolute zero, and factoring in that since you’re no longer commuting your gas bill will go down dramatically?

What about income? With time to spare, could you replace a decent percentage of your income by picking up some work in the gig economy? Or could you pick up some other, more traditional part-time job while you look for a job to replace your income? What about unemployment income?

These types of factors are why I’m a believer in carrying much less than six months, and more like two to three months, of your current expenses as your emergency fund. Of course, that’s with the caveat that instead of putting away money in your emergency fund, you’re instead investing that money.

A two-month or three-month emergency fund covers you for around 95% of common emergency fund expenses, like car and home repairs, insurance deductibles, a short to medium term layoff from work, or buying a last-minute flight to attend a funeral.

Putting another three months of expenses aside might cover you for 98% of emergencies. So, while you may have enough to get through a layoff, you would likely not have enough to cover a long-term medical condition that eliminates your ability to work.

In my opinion, since there’s only a small chance of something like that happening — not to mention other ways to protect against this, such as disability insurance — covering that limited risk isn’t worth the opportunity cost of having three extra months of expenses locked away.

At the end of the day, you have to think through the equation yourself. Define your own purpose for carrying an emergency fund, and then work through your worst-case scenarios — as well as the specific actions you can take if those were to happen.

Where Should You Put Your Emergency Fund?

The most common place to put an emergency fund is in a high-interest savings account.

I prefer to use a separate account and a different bank than my checking account. That’s not because I can get a higher interest rate, but because I don’t want to have easy access to my emergency fund. I want it to be used in emergencies only, and having it one instant transfer away makes it more tempting in non-emergency situations.

A solid choice of bank for your emergency fund is CIT Bank, which carries one of the nation’s highest interest rates and has a minimum initial deposit of only $100.

How To Build Your Emergency Fund Fast

When you’re trying to build up an emergency fund, there are two ways to do so:

- Spend less.

- Make more.

When you spend less, not only are you able to put more money into your emergency fund, you also reduce the total amount you need to save. For example, say your goal is to build a three-month emergency fund and your average monthly expenses are $5,000. This means saving a total of $15,000.

Now, say you were able to reduce your expenses by $1,000 a month, to $4,000. You’re now able to put more money away but, just as importantly, you only need to save $12,000 to hit your goal.

At this point, the big question becomes: can you cut $1,000 (or even more) from your average monthly expenses?

While familiar tips like bringing your lunch to work or cutting out lattes do indeed reduce your monthly expenses, to cut $1,000 or more in a short amount of time you’ll need to focus on big wins, which are typically found in major expense categories like housing, interest payments, transportation and food.

- Housing: While moving may be off the table for many people, refinancing your mortgage, finding a roommate, and cutting down on your home insurance costs are smart ways to save quickly.

- Transportation: Shopping around for auto insurance, refinancing your auto loan, and trading down in car value can help you save fast.

- Interest: Your first priority when it comes to reducing the amount of interest you pay each month is eliminating high-interest debt. Beyond interest payments, refinancing your debt via debt consolidation can also help reduce costs.

- Food: Eliminating eating out and optimizing your grocery budget will get you the most savings within your food budget. This is often difficult, but it can be helpful to remind yourself that cutting these things out is a temporary action — you don’t have to give them up forever.

Making More Money

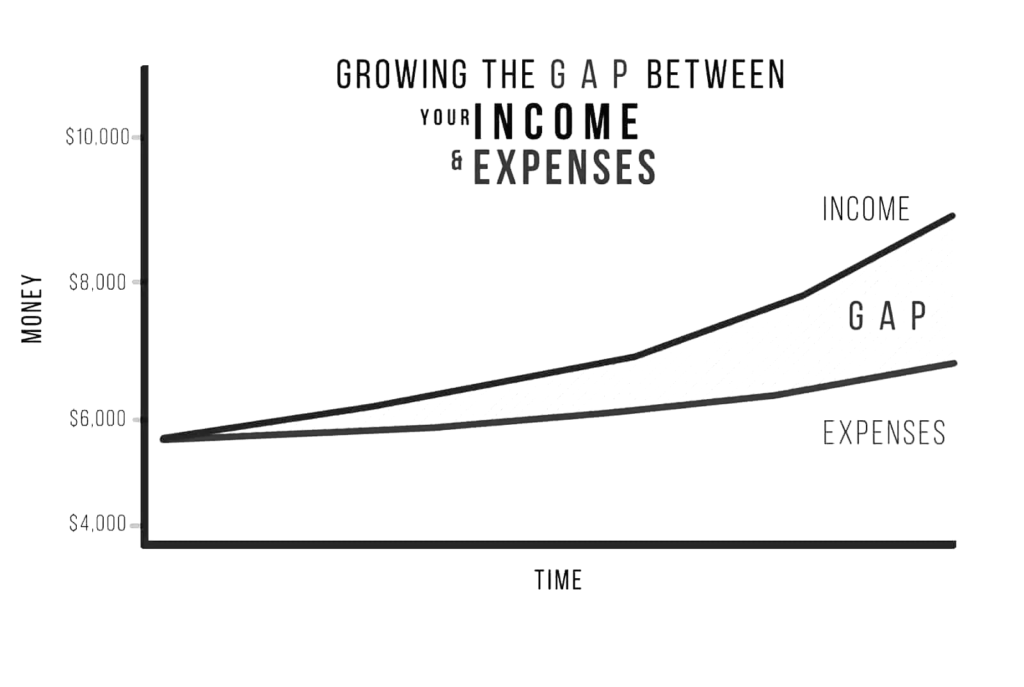

One of the success principles often talked about on this site is “Growing the Gap.” The idea is to make the gap between your income and expenses as wide as possible.

The best way to grow the gap, and therefore increase how much you’re able to put away towards your emergency fund, is to decrease expenses and increase income.

Using our previous example, let’s say your goal was to build a $12,000 emergency fund. If you were to save $1,000 a month towards that goal, it would take a total of 12 months. However, if you increase your income by $1,000 a month, to a point where you’re earning $6,000 a month and spending $4,000 a month, your gap between your income and expenses would be $2,000. Now the time needed to reach your goal is only six months.

What’s powerful about making more money is that increasing your income often gets easier the more you work on it. As an example, say you’re a beginning freelance writer making $1,000 a month. As you continue to build your portfolio and your skills in freelance writing, you can earn more money.

Growing your income is how it’s possible to achieve what once was a 12-month goal in as little as six months or less.

Here are some suggestions for getting started:

- How to Make Money From Home

- Highest Paying Gig Economy Jobs

Emergency Fund FAQ

Should you invest or build up an emergency fund?

There’s no question that you’ll benefit from a small safety net (let’s say $1,000) to protect you against unexpected expenses. Once that fund is in place, is it better to build up your emergency fund or invest? First things first: this doesn’t have to be an either/or question.

Specifically, there’s no rule that says you can’t do both at the same time. For example, by investing in your 401(k) up to the employer match and then using whatever is left over to build an emergency fund. Yes, this means it will take longer to achieve a fully-funded emergency fund. But you’ll also be taking advantage of the “free money” a 401(k) match has to offer.

Whether it makes sense to more aggressively invest or build your emergency fund comes down to which approach benefits you the most. To make that evaluation, go back to your purpose for having an emergency fund in the first place.

For example, if the purpose is to take advantage of opportunities in your career, such as launching a new business venture in the future, you might want to prioritize building up an emergency fund. If your purpose is to simply have some cash set aside for peace of mind, you might lean towards investing more, even utilizing a more advanced strategy like building up your emergency fund via a Roth IRA.

Can you use your Roth IRA as an emergency fund?

One of the most important concepts to understand for building long-term wealth is that retirement accounts like 401(k)s and IRAs are “use it or lose it” accounts. Each year, there’s only so much you can invest in such an account. If you miss that amount in a given year, there’s no way to recoup it.

When it comes to Roth IRAs specifically, a rule worth knowing is that you can withdraw contributions at any time tax and penalty-free. The downside though is that once withdrawn, you can’t put that money back into the account.

Overall, I like using a Roth IRA as an emergency fund in two scenarios.

(1) For someone just starting out, who wants to both invest and build up their emergency fund. A strategy here would be to save $500 a month in a savings account and $500 a month in a Roth IRA, invested in cash at first. Once the emergency fund is fully-funded in a savings account, then move that cash to a more appropriate investment, such as stocks.

(2) For those further along in their personal finance journey, who have built up a nice sum in their Roth IRA. In this case, they could use their Roth IRA as a backup to a smaller emergency fund that they carry in cash. The latter is what I do. I only carry about two months of living expenses in an emergency fund at any time, knowing that I have over a decade of fully-funded Roth IRA contributions for both myself and my wife as a last resort.

How do I start an emergency fund with no money?

The key to starting an emergency fund when you’re living on a tight budget is recognizing the value of small wins. It might seem insignificant, but if you only have one penny to stash away, then do it. Saving whatever you can — even if it’s literally “just” cents — is the first step to building the habit of saving.

Taking the intentional action of designating a portion of your income for a specific purpose — whether that’s an emergency fund or an investment account — helps you change the way you think about your relationship to money (and how you use it). So it’s OK if you have almost nothing to save right now. Start where you are and build up slowly.

To help with this, consider using a service like Chime, which offers free online bank accounts. Chime has two valuable features — roundups and paycheck withdrawals — that can make saving small amounts easier. With the roundups feature, Chime rounds up your debit card purchases to the nearest dollar and sets aside the “spare change.” With paycheck withdrawals, a set portion of your income is automatically put into savings each pay cycle.

How can you make sure to only use your savings in a true emergency?

The best way is to create one degree of separation between you and your rainy day fund. For example, if you place your money in an online savings account, keep it separate from your primary bank. Savings accounts don’t have debit cards because federal law limits the number of fee-free withdrawals you can make each billing cycle, so keeping your emergency account in its own silo makes it harder to spend that money, as you have to physically transfer it from one institution to another.

The Bottom Line On Emergency Savings

If you don’t have an emergency fund, there’s no better time to start than today. Even making your first $10 deposit will allow you to go to bed tonight with more financial stability than when you started the day. As that amount grows, you’ll enjoy the peace of mind that comes with knowing that unexpected events aren’t going to push you into financial catastrophe.

From there, keep building. Every step you take will make the next step easier. And I promise that before too long, saving money will become something you take pride in rather than something you dread.

And once you do reach your savings goal, that’s when things get exciting. Not only will you sleep better, but you’ll be on your way to accomplishing bigger and better things with your money, knowing that you have a solid foundation in place.